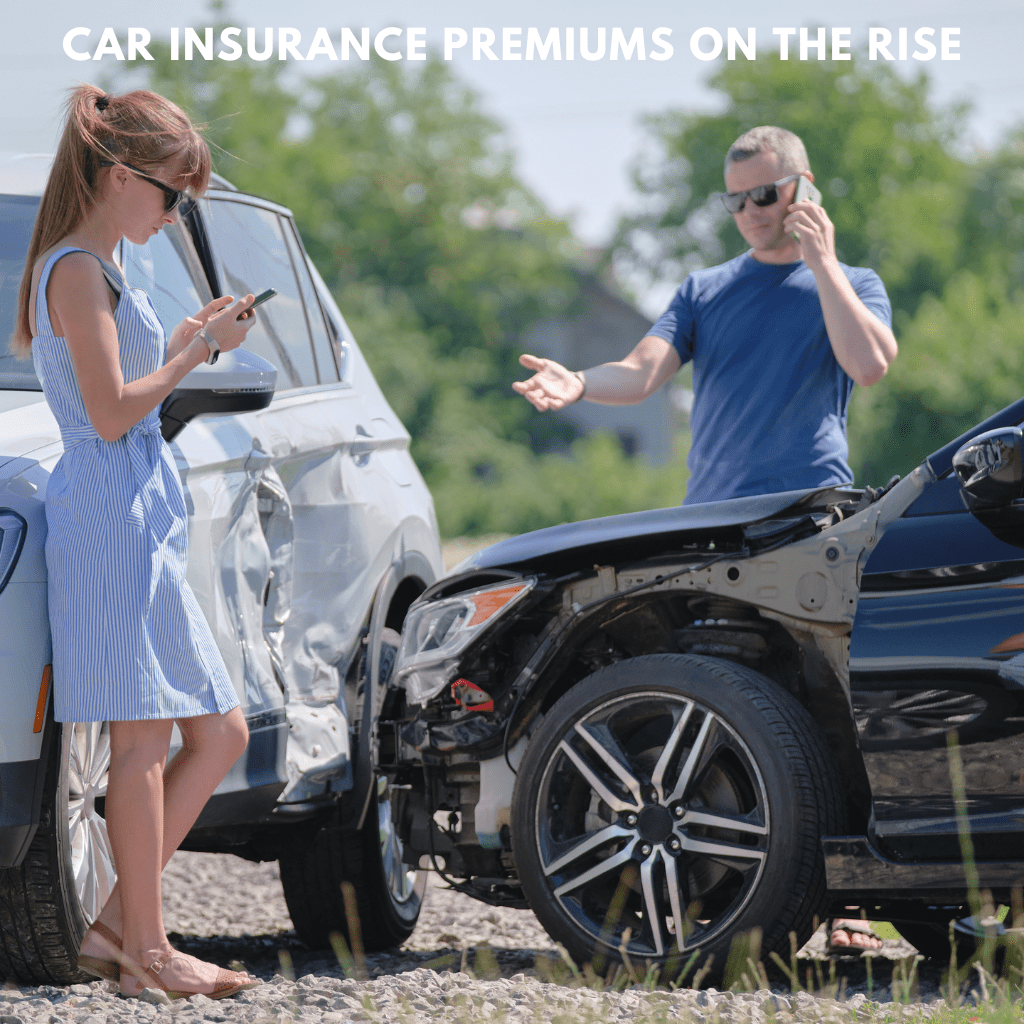

If you’ve noticed a steady increase in your auto insurance premiums lately, you’re not alone—and the culprit might surprise you. Beyond inflation and other common factors, tariffs on imported vehicle parts have been quietly making waves in the insurance industry. These tariffs increase costs for insurers when repairing vehicles, and those expenses inevitably trickle down to consumers. Let’s unpack how this domino effect works.

The Role of Tariffs in Auto Insurance

Tariffs are essentially taxes imposed on imported goods, including vehicle parts from foreign manufacturers. These parts are vital for repairing cars following an insurance claim. When tariffs hike the prices of these parts, repair costs surge. For instance, a bumper sourced from overseas might now cost insurers significantly more than it did a few years ago. These added costs put a strain on insurance providers, who then factor them into the premiums paid by policyholders.

The Ripple Effect on Repairs and Claims

Vehicle repairs are one of the largest costs associated with auto insurance claims. Imagine you’re in a minor fender-bender: your car requires a new tail light assembly that’s manufactured abroad. Due to tariffs, the cost of that assembly spikes, inflating the overall repair bill. Since insurers are footing the bill for claims like these, the increased repair costs contribute directly to higher premiums for all policyholders.

Consumers Feel the Pinch

While tariffs aim to protect domestic industries, they also have unintended consequences for everyday drivers. Higher repair costs mean insurance providers must balance their books by adjusting premiums. Unfortunately, this means the average driver may see their insurance rates climb—even if they haven’t filed a claim or made any changes to their policy. For households on tight budgets, these increases can create added financial strain.

What Can You Do?

As tariffs continue to influence auto insurance rates, it’s wise for drivers to be proactive. Here are some tips:

- Shop Around: Different insurers may absorb costs differently, so comparing rates could save you money.

- Maintain a Safe Driving Record: Avoiding accidents and claims can make you eligible for discounts, easing the burden of rising premiums.

- Consider Usage-Based Insurance: Some policies adjust rates based on how much or how safely you drive, which might lower costs.

- Stay Informed: Understanding the economic factors affecting your premiums, like tariffs, can help you make smarter decisions.

Looking Ahead

While tariffs aim to strengthen domestic manufacturing, their ripple effects on industries like insurance remind us that every policy change carries unintended consequences. As tariffs persist, insurers will continue grappling with increased repair costs—and, inevitably, so will consumers. For now, staying informed and exploring your options can help you navigate these rising premiums without breaking the bank.

Auto insurance premiums might feel like yet another cost that’s climbing for reasons beyond your control. But knowing why these increases are happening is the first step toward managing them more effectively. What do you think—are tariffs a necessary measure, or do their side effects outweigh their benefits? I’d love to hear your thoughts!